You are reading a complimentary report. To find out more about our services,

You are reading a complimentary report. To find out more about our services,

Executive Summary

Republican Sweeps Benefitted Real Estate, Materials & Utilities

Fullscreen Fullscreen |

- We still assign a contrarian 55% chance that Trump will win the presidency in November, which will most likely result in a full Republican Sweep. A Harris victory is not unlikely and would result in a mixed or Republican Congress – though the odds of Democrat Sweep are rising.

- Equity returns are usually softer after a change in incumbency. Sector leaders turn into laggards when policy changes in response to a shift in the party occupying the White House.

- A near-term economic slowdown favors Defensives. We favor Health Care no matter the election outcome, while we like Utilities under a Republican White House.

- The Republican policy platform favors Real Estate, Materials, Energy, Financials, and Industrials. A Democrat victory means policy will most likely be restricted by gridlock, and the status quo benefits Health Care, and Information Technology.

- On a rotation basis, Real Estate and Health Care are opportunities.

- On a composite factor basis, Health Care, Utilities, and Communication Services are most expected to rebound over a tactical horizon.

Chart 1

Volatility Will Rise Into Election Day

| Fullscreen | Interactive Chart |

The recent spike in volatility was the start of the election season, which will only accentuate the normal ructions often experienced in the months of September and October more generally (Chart 1).

Investors must also contend with recession fears which have gained traction in response to the slight rise in the unemployment rate in 2024. In fact, BCA already expects a recession to materialize at the end of year or in early 2025, which justifies favoring Defensive over Cyclical equity sectors.

The election will impact the economy and market, especially if Trump wins, which would result in drastic policy change. Over a four-year period, we assess Trump’s proposals as fiscally stimulating and mostly inflationary.

A Trump presidency would favor sectors like Energy, Financials, Industrials, Materials, and Real Estate – all which have ties to current proposed policies. Sector performance under a Harris presidency will depend on the results in Congress.

From a defensive standpoint, Health Care and Utilities are our picks for downside protection against a looming recession and amid a changing policy backdrop.

Equities And Elections

In the final months of an election cycle, equities underperform relative to non-election years. This extends into Q1 of the following year (Chart 2).

Once the election results are clear, equities recover. Hence, the volatility around the day of the elections should be faded. That is not to say the election is market neutral. A distinction between a Trump or Harris win is still important. Incumbency matters to markets. If party control of the White House changes, national policy changes too.

Equity returns are higher after the election when the incumbent party wins the presidential election (Chart 3). Incumbent parties define the current status quo and their policies promise a continuation of current trends – the source of risk shifts from internal to external surprises. Markets have less uncertainty to price and are less volatile. Lower uncertainty is good for risk assets. By contrast, a change in incumbency results in weaker returns.

Chart 2

Equity Returns Are Weaker In Election Years

| Fullscreen | Interactive Chart |

Chart 3

Incumbency Continuity Is Good For Stocks...

| Fullscreen |

Chart 4

...But When Incumbency Changes, The Worst Sectors Become The Best

| Fullscreen |

Generally, a change in political leadership also leads to a change in market leadership. Outperforming sectors benefiting from the incumbent party underperform. Policy headwinds that created sector laggards are more likely to fade. In fact, the three sectors that performed worst during a party’s mandate start to outperform the three that performed best if the challenger party takes over the executive (Chart 4, top panel).

In elections where the ruling party remains in power, the market leadership change becomes a lot less significant (Chart 4, bottom panel). By this measure, Materials, Energy, and Consumer Staples would be favored today, while Financials, Information Tech, and Communication Services would

not.

Bottom Line: Equity returns are usually softer after a change in incumbency. Sector leaders turn into laggards when policy changes in response to a shift in the party occupying the White House.

Which Defensives?

Chart 5

Utilities Are The Best Defensive Under A Republican President

| Fullscreen | Interactive Chart |

Historically, Health Care is the best performing defensive sector immediately following a Democrat victory in the presidential election (Chart 5, top panel). Meanwhile, when a Republican is elected, Utilities is the best defensive sector (Chart 5, bottom panel).

Health Care offers the best prospects in the near term, regardless of the election outcome.

Structural tailwinds include declining mortality relative to morbidity, aging demographics, record numbers of innovative drugs coming to market, generative AI, and discounted valuations, as outlined by BCA’s US Equity Strategy.

We also favor Utilities over Consumer Staples. Both are defensive, though consumers have demonstrated a reluctance to spend, given a high share of top-line misses among companies, reduced volumes, and increasingly price-conscious behavior.

While consumers show some signs of recovery, Utilities are a bond proxy that outperforms during recession or when rates are declining or low. The sector will also benefit from rising demand for energy by data centers, a play on the generative AI theme.

Bottom Line: In the near-term, choose Health Care and Utilities amid recession risks. Both sectors will also benefit from industry tailwinds.

Trump Is Still Our Pick (But Conviction Is Low)

Chart 6

Harris Has Generated A Predictable "Nomination Bounce"

| Fullscreen | Interactive Chart |

The election is a dead heat as we go to press. We now assign a 55% chance that Trump will win the presidency in November, an out-of-consensus view.

True, Harris has a strong tailwind as the head of an incumbent party after only four years. Since taking President Joe Biden’s place as the Democratic nominee, Harris has generated a predictable “nomination bounce.” However, she remains statistically tied with President Trump, including in swing states (Chart 6).

The economy and global stability are marginally deteriorating, so Harris faces hurdles in September and October that the mainstream media and financial markets are not yet computing.

The loss of an incumbent president advantage with Biden dropping out, the uptick in unemployment in contested states, and the lackluster polling among key demographics, lead us to maintain our view of a Trump victory in the White House, though we downgrade his odds to 55% from 60%.

We also break down the 55% probability for Trump and Republicans into 50% odds of a full sweep (White House + both chambers of Congress), and 5% odds of a GOP win with a mixed congress (Diagram 1), given the Republicans’ cyclical advantage in the Senate and House.

In contrast, a Harris victory will likely result in a Republican or mixed congress, our second most likely outcome at 25%.

The chance of a Democrat Sweep is lower at 20%.

Diagram 1

Election Outcome Probabilities

| Fullscreen |

Under a Republican Sweep (50% probability), we would expect:

Chart 7

The Budget Deficit Tends To Rise Under Republicans

| Fullscreen | Interactive Chart |

- Wider budget deficits: Under a full sweep, the 2017 tax cuts will be extended, corporate taxes will marginally decrease, and personal taxes will also fall, potentially by a large amount. Republicans will cut some spending but will not reform entitlements and will not fully offset their tax cuts since their objective is to stimulate rather than restrain the economy. Historically, Republicans have increased budget deficits (Chart 7), especially with full control of both chambers.

- Higher long-term inflation: Major increases in the deficit will be inflationary in the long term, though possibly not in the short term if a recession emerges, as we expect. The dollar will rise in a recessionary environment and may stay elevated if the rest of the world does not match American’s stimulus.

- Greater labor shortage: Restrictions on immigration will reduce the supply of labor in the US. High demand for labor increases real wages. The primary impetus of the Trump movement is to curb immigration. Trump failed to do so in his first term, but he will not fail again if he wins another full sweep.

- Higher oil volatility: Republicans will not restrain Israel and will act hawkish toward Iran by enforcing oil sanctions (unlike Biden). Oil shocks originating in the Middle East will grow more likely.

Chart 8

Trump Is Willing To Raise Tariffs Substantially

| Fullscreen |

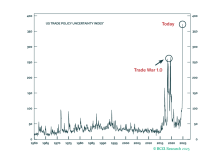

- Higher tariffs on China: Potential tariffs of up to 60% against China have been proposed. There is a debate about Trump’s ability to raise tariffs that much, but he is willing to raise them substantially (Chart 8). The US trade deficit may fall in the short run if imports contract during a recession, but over the long run, trade deficits would remain large. Tariffs would shift deficits away from China to other countries.

- Stronger housing prices: Republican policy favors single-family homes over dense construction. Immigration curbs will constrain developers’ profit margins and hence housing supply. Inflation will also contribute to housing price growth.

- Elevated policy uncertainty: While global policy uncertainty is escalating regardless of Harris or Trump, full Republican control will allow Trump to pursue unorthodox policy. Trump would also be a second-term president ineligible for reelection so he would have a large risk appetite for disruptive foreign and trade policy.

Under a Harris Presidency (45% probability), we would expect:

- Fiscal tightening: Domestic policy would be gridlocked, unless Democrats win a sweep. Harris would allow the Trump tax cuts to expire for high-income earners, but Republicans in Congress would not grant major spending increases. Congress would not stimulate the economy until after a recession clearly materialized. Additionally, policy uncertainty would fall, since any major legislation would need to be bipartisan and hence moderate in ideology. Major policy risks would stem from outside the US not inside. This would be a positive environment for low-beta assets.

- Brinksmanship with Russia: Harris’s election would complete the triumph of the Washington political establishment, while Trump would fall, and the GOP would go into the political wilderness. The Democratic Party would double down on the foreign policy agenda, leading Europe and the West to support a new Ukrainian offensive. Russia would need to resort to energy shocks or nuclear brinksmanship to meet its objectives of keeping Ukraine weak, neutral, and out of NATO. This combination would support safe havens.

- Less volatility in the Middle East: Democrats would pursue engagement with Iran and would try to contain Israel. Oil shocks may still occur, if Iran pursues nuclear weapons anyway, or if Russia disrupts energy supply in a significant way.

The economic environment in the US will differ under both scenarios, yet regardless of the outcome, we expect defense spending to remain elevated, hawkish policy against China, and monetary policy to be either neutral or dovish in 2025. Neither president would cut defense spending amid heightened geopolitical competition.

Neither president would reduce pressure on China without first negotiating trade concessions.

Neither president would appoint a hawk to replace Chairman Powell. And Powell will need to respond to a recession, no matter who occupies the Oval Office.

New Government: Which Sectors To Choose?

A Trump-led Republican sweep is our base case. Let’s explore the sectoral implications of this outcome as well as those from a gridlock with the Democrats in the White House. Appendix Table A1 shows sector performance under both assortments in the two branches of government, as well as the performance under various economic scenarios we expect under either administration.

A Republican Sweep

In past Republican sweeps, Real Estate, Materials and Utilities were the best-performing sectors (Chart 9A).

Real Estate is poised to benefit under the Republican 2024 platform. Policies include lowering borrowing costs for homebuyers through tax incentives and support, as well as protections and single-family zoning would boost property prices. Decreases in demand stemming from immigration restrictions would be offset by labor shortage among homebuilders, further decreasing supply. Neutral to dovish monetary policy in the near-term will boost performance.

Materials also benefit from Trump policy. While immigration and trade restrictions under Trump may be negative, the sector will benefit from a push to reshoring US industry alongside the reinstating of “Trump’s Deregulation Policies.”

Last, the Energy sector will be poised to grow under a GOP sweep. Beyond regulatory easing, Republicans emphasize the need to increase domestic production of oil and gas, and support significant energy infrastructure investments in pipelines, power grids, and export facilities. Tax incentives for domestic energy producers will also improve the profitability of these firms. Note that a substantial increase in drilling may bring down energy prices and dampen outperformance.

The Republican 2024 platform is not opposed to renewable energy, instead it emphasizes overall production. Foreign policy on the Middle East would also favor energy producers in the Americas.

Table 1 shows major Republican policy proposals, and which sectors will believe will be impacted. We favor these sectors based off a qualitative assessment of potential tailwinds emanating from policy. On balance, sectors like Energy, Materials, Financials, and Industrials stand to benefit most, especially if recession does not happen or is already priced.

If No Republican Sweep, Then...

The most likely alternative government in this election is a Harris presidency with congressional gridlock. Information Technology, Health Care, and Financials have performed best under this type of government (Chart 9B).

Chart 9A

Republican Sweeps Benefitted Real Estate, Materials & Utilities

| Fullscreen |

Chart 9B

A Harris Win And Congressional Gridlock Favor Tech, Health Care & Financials

| Fullscreen |

Table 1

Republican Polices And Sector Impacts

| Fullscreen |

Harris has released an economic wish list consisting of price controls and social spending. She will likely uphold Biden’s policy proposals. Biden has long championed bringing corporate tax rates back to 28%, and now Harris has reinforced the party support for a tax hike. Additionally, Artificial Intelligence regulatory restrictions regarding data privacy will grow, and so will anti-trust enforcement. Consequently, the political environment for Information Technology will pose barriers if Democrats are unconstrained, and may not be beneficial to returns.

Regulation would also extend to the financial sector. Consider what Harris would do if given a full sweep: higher corporate taxes, capital gains taxes, financial transactions taxes, and potentially even unrealized gains taxes would dampen profits for this industry due to additional costs incurred to meet new standards. Harris could not pass tax hikes without Congress but then she would be more likely to use executive decrees aggressively to enforce tax collection and increase regulation on Financials. Republicans favor reducing capital gains and corporate taxes, easing lending standards, and rolling back some regulatory measures under the Dodd-Frank Act. A gridlock in congress would be neutral, as Democrat ambitions will be contained by the legal and legislative process.

Under gridlock, Health Care once again presents the best opportunity – Democrats seek to enhance the Affordable Care Act (ACA), which would boost demand for Health Care services and products by increasing the number of benefit recipients. A Republican sweep would not be as beneficial – Republicans are unlikely to make the mistake of trying to repeal the ACA again, but they would cut subsidies and social spending. Note, however, that Harris’s implementation of Biden’s drug price controls would be negative for Big Pharma’s profits, but Republicans would repeal or refuse to implement them.

Note that the rising probability of a Democrat Sweep would mean more of their ambitious platform passing into law. Historically, Information Technology and Real Estate were outperformers. Yet Democrat regulations, enforcement of anti-trust laws, and tax hikes will act against these sectors. Health Care will face headwinds from regulations on pharmaceuticals and price caps. Industrials and Energy should still benefit from Democrat reshoring efforts, infrastructure investments, and energy shocks emanating from hawkish policy with respect to Russia-Ukraine. Table 2 outlines major Democrat policy and the sector implications.

Table 2

Democrat Policies And Sector Impacts

| Fullscreen |

Bottom Line: Historically, a Republican sweep favors Real Estate and Materials, while their policy agenda favors Energy, Materials, Financials, and Industrials. Recession risk favors Utilities as a tactical winner.

If Democrat policy remains constrained in Congress, Information Technology and Financials will outperform if a recession is avoided. Health Care should be a short-term winner. Be cautious of these sectors under a Democrat Sweep government.

Rotating Around The Election

Sector rotation will increase amid expanding recession risks and as the election approaches, irrespective of whether policy changes under a Trump presidency or the status quo remains under Harris.

Over the past six months, relative rotational movements have mostly oscillated between two quadrants for most sectors (Chart 10). Information Technology is the only sector in the “Leading” quadrant, though it has weakened – in line with market concerns of a bubble in generative AI related tech stocks.

Chart 10

Most Sectors Are Rotating Between "Improving" And "Lagging"

| Fullscreen |

Real Estate, Financials, and Consumer Discretionary have moved to the “Improving” quadrant from the “Lagging” quadrant, making them good candidates to beat the market going forward.

Meanwhile, Health Care resides in the “Weakening” quadrant but appears to be making a play toward the “Leading” quadrant.

There are some parallels to draw between now and the 2020 election but note that the introduction of the COVID-19 vaccine was also a major vector for rotation (Chart 11). Information Technology was leading three months prior to the election but moved to “Weakening” three months afterward. Several other sectors also rotated between improving and lagging quadrants in 2020, like Utilities, Real Estate, Industrials, Financials, Communication Services, Materials, and Consumer Staples.

Chart 11

Some Sector Rotation Parallels With 2020 Election

| Fullscreen |

Interestingly, Defensives and Cyclicals have been trading places for the past six months, moving between bearish and bullish quadrants (Chart 12). Investors are still uncertain about a recession. Election uncertainty will compound these doubts.

Chart 12

Defensives Vs. Cyclicals: Investors Are Still Uncertain About Recession

| Fullscreen |

In 2020, election uncertainty was elevated too. Cyclicals faded and Defensives came into the spotlight post-election (Chart 13). While Biden won the election, his policy agenda differed from that of Donald Trump, which resulted in a break of policy continuity and a rise in uncertainty. In 2021 the risk-on and reflation rally occurred.

Chart 13

In 2020, Cyclicals Faded, Defensives Shined Post-Election

| Fullscreen |

Though some of our sector picks are Cyclicals, we assign more weight to recommending Defensives now, considering the highly uncertain macro and political backdrop.

Bottom Line: Real Estate and Health Care stand out as opportunities. Defensives will take favor over Cyclicals post-election, especially under a Democrat gridlock.

Sector Screening With BCA’s Equity Analyzer

BCA's Equity Analyzer applies a top-down approach to bottom-up stock picking. The service uses a variety of quantitative metrics to rank individual stocks and presents this information in an easy-to-use web application. By quantifying and combining numerous return factors, Equity Analyzer enables its users to find stocks with winning characteristics.

Now that we have a better view on which sectors we expect to outperform under a second term Trump presidency, we leverage BCA’s Equity Analyzer platform to gather further insights on a sector-by-sector basis.

The BCA Score, which ranges from 0% to 100%, is based off a 30-factor model which is grouped into seven composite factors (Table 3). The model favors low volatility, strong momentum, and high-quality stocks. The higher the BCA Score, the better.

Table 3

Equity Analyzer Composite Scoring By Sector

| Fullscreen |

Most sectors are trading near their six-month post-election BCA Score average including defensives like Consumer Staples, Health Care, and Utilities. Communication Services and Utilities are the furthest below their post-election BCA Score average – indicating they have greater reversion over other sectors.

Investors looking for specific factor exposure should consider sectors where current Composite Scores (dot marker) are lower than their six-month post-election Composite Scores (x marker). Examples include:

- Quality: Financials, Real Estate, Health Care, Utilities and Communication Services.

- Safety: Energy, Communication Services

- Value: Real Estate, Utilities

- Payout: Industrials, Health Care, Communication Services

In Equity Analyzer, we have set up three screeners for high BCA Scoring stocks under different filters. For all the below screeners, we select the following default criteria:

- Stocks that are traded on US exchanges and domiciled in the US

- Stocks with a BCA Score above 50%

The above filters can be changed according to your investment preferences. These screens are dynamic in nature and updated on daily basis.

US Large Cap Defensives (Consumer Staples, Health Care ex- Biotech, Utilities, Chart A1)

- Market Cap = $5 billion +

- Select Top 10% based on Market Cap (USD) by sector

- Select Top 5 based on BCA Score by sector

US High Quality - Real Estate (Chart A2)

- Market Cap = $5 billion +

- Quality Score = 70% +

- Select Top 10 based on BCA Score

US Payout - Industrials And Communication Services (Chart A3)

- Market Cap = $1 billion +

- Payout Score = 70% +

- Select Top 10 based on BCA Score

We back test these three screens with quarterly rebalancing to highlight their performance relative to the broad market.

- CAGR: 11.17%

- Sharpe Ratio: 0.84

- Max Drawdown: 30.98%

- CAGR: 12.29%

- Sharpe Ratio: 0.77

- Max Drawdown: 42.31%

US Payout – Industrials and Communication Services

- CAGR: 11.63%

- Sharpe Ratio: 0.68

- Max DD: 40.87%

Bottom Line: Composite factors for Health Care, Utilities, and Communication Services are expected to rebound toward their six-month post-election factor scores once the election is over, presenting an investment opportunity for investors looking for specific factor exposure over a tactical horizon.

Investment Implications

- The macro-economic near-term environment will suppress returns for cyclical sectors. Defensives present a better option.

- Among defensives, we favor Health Care and Utilities. Historically they outperform around elections, and the policy outlook is neutral-to-bullish regardless of the electoral outcome.

- Looking at sector historical performance under a Republican-only government, the best sectors are Real Estate and Materials.

- For a Democrat victory in the White House without control of Congress, Health Care is the best sector. Health Care has strong fundamentals, and Democrat policy will further drive outperformance. Information Technology and Financials have historically benefited, though major regulatory action by Democrats is on the table if Republicans cooperate.

- Under either administration, Energy will underperform in the short-term. Hyper-cyclical sectors will not escape the forthcoming recession. However, we are bullish on Energy over a strategic horizon. Oil shocks emanating from the Middle East or Russia, or both, will cause prices to tick higher.

- Other hyper-cyclical sectors like Materials and Industrials, will also suffer during a recession, but a Republican sweep could result in less downside risk for these sectors.

- On a rotation basis, Real Estate and Health Care are standouts.

- For investors looking for specific factor exposure based on quality, value, payout, and safety, Health Care, Utilities, and Communication Services are below their six-month post-election average BCA Composite Scores, indicating greater reversion in coming months.

Max Malak

Research Associate

max.malak@bcaresearch.com

Guy Russell

Associate Editor

guyr@bcaresearch.com

Pratik Bhanuse

Quant Analyst

pratik.bhanuse@bcaresearch.com

Appendix

Table A1

Median Sector Returns Under Potential Economic And Political Conditions

| Fullscreen |

Chart A1

Factor Analyzer: US Large Cap Defensives

| Fullscreen |

Chart A2

Factor Analyzer: US High Quality - Real Estate

| Fullscreen |

Chart A3

Factor Analyzer: US Payout - Industrials And Communication Services

| Fullscreen |