You are reading a complimentary report. To find out more about our services,

You are reading a complimentary report. To find out more about our services,

Audio Summary

Executive Summary

China Has Not Yet Deleveraged

Fullscreen Fullscreen |

- Symptoms of a liquidity trap for Chinese households are appearing.

- A high debt servicing burden along with downbeat sentiment will curb demand for credit among households and businesses.

- Our proprietary indicators for the marginal propensity to spend among households and enterprises continue falling.

- China’s industrial economy will underwhelm. Consumer spending on services will grow, but at a slower pace than in the past. Consumer stocks are vulnerable because of their lofty valuations.

- As we previously argued, there has been a paradigm shift in Beijing’s approach to policy stimulus. Managing downside risks to the economy in both the short and long term is now the government’s priority.

- In addition, the scope for monetary easing is currently limited due to a depreciating currency.

- All in all, authorities will be slow to introduce large stimulus. Hence, for now, China-related financial markets are set to fall further.

There is potential for a further decline in commodity prices, EM risk assets and global cyclicals. Stay put.

Feature

China’s reopening trade turned out to be a “buy the rumor, sell the news” type of investment play. Chinese financial markets have performed very poorly since February 1st (Chart 1).

Interestingly, not only did China-related plays – like industrial metals and commodity currencies – roll over on February 1st, but also the global equal-weighted equity index peaked on the same date (Chart 2). Remarkably, Emerging Asian ex-China currencies topped out, and the broad-trade-weighted US dollar bottomed on February 1st as well (Chart 2, middle and bottom panels).

Chart 1

Chinese Markets Peaked On February 1

| Fullscreen |

Chart 2

Various Global Markets Also Peaked On February 1

| Fullscreen |

Chart 3

China: PMI New Orders Have relapsed

| Fullscreen |

We have maintained our negative bias toward Chinese and China-related assets despite the reopening. In our 2023 outlook for China, published on December 14, we argued that China’s recovery would be driven by consumers, especially spending on services, while its industrial segments would disappoint. There is now overwhelming evidence to suggest that this is what has transpired (Chart 3).

This report discusses the causes of such poor performance, the outlook of the Chinese economy, as well as our proposed investment strategy.

Is China Facing A Liquidity Trap?

A liquidity trap is a condition that occurs when low borrowing costs are unable to boost credit demand and economic growth, i.e., when low interest rates become ineffective.

Chinese households are showing symptoms of a liquidity trap. They are presently reluctant to borrow and purchase real estate even though mortgage rates have fallen to a 14-year low (Chart 4). On the contrary, households are repaying their mortgages (Chart 4, bottom panel). At this point, a small reduction in mortgage rates is unlikely to alter these dynamics considerably.

The basis is twofold: (1) households already have a large debt burden (Chart 5, top panel); and (2) the carry trade in housing is over (Chart 5, bottom panel).

Chart 4

Households Are Paying Down Mortgages

| Fullscreen |

Chart 5

Reasons Why Households Are Reluctant To Borrow

| Fullscreen |

When the pace of house price appreciation was consistently above mortgage rates i.e., when the carry was positive – there was a strong appetite for mortgages. As people are no longer expecting the rate of property price appreciation to exceed mortgage rates, housing demand has downshifted considerably.

Unless household expectations for home price appreciation rise substantially, they will be reluctant to borrow and purchase property. Hence, the key driver of residential property sales in China remains the expected pace of home price appreciation, not mortgage rates. Consequently, a moderate reduction in borrowing costs is unlikely to alter Chinese households’ current aversion to real estate.

Meanwhile, mainland companies are among the most indebted in the world (Chart 6). Saddled with a great deal of debt and faced with a lack of government stimulus and weak demand, businesses are unlikely to invest, expand and hire.

Even after we remove local government financing vehicles (LGFVs) that are classified as enterprises, the level of corporate debt is considerably higher in China than in the US (Chart 6). We have recently published an in-depth report on LGFV debt.

The BIS estimates that debt servicing costs (interest and repayment of principal) for Chinese households and companies stand at 21% of their income. This ratio is higher in China than in many other economies (Chart 7).

Chart 6

Chinese Companies Are Highly Indebted

| Fullscreen |

Chart 7

The Debt-Service Ratio for Chinese Households And Companies Is Elevated

| Fullscreen |

A high debt servicing burden along with downbeat sentiment will curb the demand for credit. Our proprietary indicators for the marginal propensity to spend among households and enterprises continue falling (Chart 8).

Bottom Line: There is evidence to suggest that China is experiencing some sort of liquidity trap.

As a result, marginally lower interest rates are unlikely to be effective in boosting growth.

The Growth Outlook

Multiple forces will continue to dampen China’s post-pandemic economic recovery:

- There was a lack of fiscal transfers to households during the lockdowns. Unlike the US, household income growth in China was very weak during the pandemic (Chart 9, top panel). This dynamic explains the relatively more muted post-lockdown consumer rebound in China.

Chart 8

The Marginal Propensity To Spend Is Low And Falling

| Fullscreen |

Chart 9

Household Income Growth And Confidence Are Weak

| Fullscreen |

- The deteriorating housing market is weighing on consumer confidence. Over the past 20 years, the wealth effect from rising house prices had a non-trivial impact on Chinese consumer confidence and, thereby, their spending. Presently, consumer confidence remains depressed, albeit above pandemic lows (Chart 9, bottom panel).

- Private investment and hiring will disappoint because of the lack of confidence among private businesses. Socio-political and geopolitical changes as well as the economic uncertainty have depressed private business sentiment.

- Since October’s Party Congress, the key word used by many Politburo members in their speeches and articles has been “struggle”. This underscores that socio-political stability and geopolitical standing – rather than economic growth – are Beijing’s priorities.

- Infrastructure spending will continue to decelerate as the special bond issuance quota for local governments this year is below its 2022 level (Chart 10).

Chart 10

Infrastructure Spending Will Decelerate

| Fullscreen |

- The revival in Chinese exports in March and April was probably an aberration. Chinese manufacturing PMI export orders have rolled over, signaling a renewed contraction in exports.

China is trying to diversify its overseas shipments away from the US and the EU. Nevertheless, this is a structural long-term process and is unlikely to lead to a near-term decoupling of Chinese overall exports from contracting global trade.

Bottom Line: China’s industrial activity will continue to disappoint. Consumer spending on services will grow, but at a slower pace than in the past.

Stimulus To The Rescue?

In our March 8 report titled A Paradigm Shift In Chinese Economic Policy, we argued the following:

- There has been a paradigm shift in Beijing’s approach to policy stimulus. The main purpose of government policy is now to manage downside risks to the economy in both the short and long term.

- In the short run, rather than producing a robust economic expansion, authorities aim to put a floor under growth and prevent a downward spiral from occurring.

- At the same time, the central government is seeking to avoid aggravating structural imbalances in the economy and financial system such as elevated indebtedness, real estate excesses and financial speculation.

In an era of “struggle”, the government is especially intolerant of excesses and bubbles that can burst at any moment. Instead, keeping the economy and financial system “grounded” will limit the downside from a potentially negative external shock. - The priority for the central government is to build economic and financial system resilience against potential negative shocks, including external threats.

Chart 11

China Has Not Yet Deleveraged

| Fullscreen |

For all these reasons, the central government in China will not rush to provide large irrigation-type stimulus.

If the economy enters a downward spiral, policymakers will stimulate, but they will not adopt a proactive policy stance.

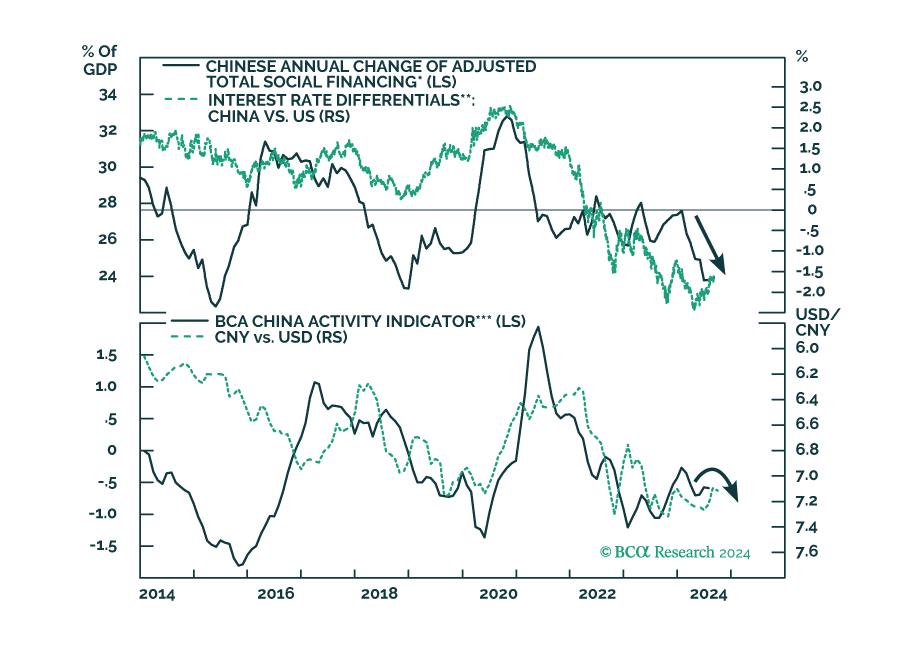

Importantly, China has not yet undergone a deleveraging process – the domestic debt-to-GDP ratio continues to rise (Chart 11, top panel). Given that credit growth remains above 10% and there are low odds that nominal GDP growth will reach double-digit rates (Chart 11, bottom panel), the debt-to-GDP ratio is set to rise further.

The failure of growth to accelerate despite double-digit credit growth confirms our long-term theme that the Chinese economy has become addicted to credit, i.e., without excessive credit growth, the economy will struggle.

In this context, the only way to boost growth is to accelerate credit growth from the current 11% to 15%, which would cause the credit and housing excesses to grow even larger. This last option is inconsistent with current policy priorities.

Finally, the scope for monetary easing is currently limited due to the depreciating currency. US inflation will prove to be sticky, and the Fed will err on the hawkish side. As a result, if the PBoC were to reduce interest rates aggressively, the yuan will weaken sharply. The latter will further depress business and consumer confidence.

Little known is the fact that last October when the CNY was depreciating rapidly, the PBoC tightened liquidity by pushing up interest rates. The top panel of Chart 12 illustrates that the PBoC withdrew liquidity/excess reserves from the banking system in October-December. Consequently, the 3-month SHIBOR interbank rate (a de-facto policy rate) rose during that period.

This spike in interbank rates led to a notable rise in onshore government and corporate bond yields. Such an upward shift in Chinese interest rates, along with the decline in US bond yields, prompted a rebound in the CNY/USD exchange rate in late 2022 (Chart 12, bottom panel).

Yet, liquidity tightening has implications for credit origination. Chart 13 shows that the excess reserve ratio leads the credit impulse. Hence, another relapse in the excess reserve ratio would herald a setback in the credit impulse.

Chart 12

The PBoC Tightened Liquidity In Q4 2022

| Fullscreen |

Chart 13

China: Excess Reserves And Credit Impulse

| Fullscreen |

In short, the PBoC is facing a dilemma: should it reduce interest rates aggressively to boost domestic demand, or should it focus on exchange rate stability?

BCA’s Emerging Markets Strategy service expects the trade-weighted US dollar to appreciate meaningfully in the coming months. This will complicate the trade-off faced by Chinese policymakers and will delay any meaningful stimulus.

Bottom Line: Our theme - that there has been a paradigm shift in Chinese policy and that authorities will be slow to introduce large stimulus - remains intact. Hence, for now, China-related financial markets are set to fall further.

Investment Conclusions

- China’s economy is ailing and is in need of substantial monetary and fiscal stimulus to recover. Yet, policymakers will be reactive rather than proactive. As a result, Chinese stocks and China-related assets will continue falling.

We downgraded Chinese investable stocks from neutral to underweight on February 1st (Chart 14) and continue to recommend underweighting Chinese investable stocks within global and EM equity portfolios.

For now, we recommend overweighting Chinese onshore shares within global and EM portfolios. This is not so much a bullish call on A-shares as it is a bearish call on the global equity index.

Chinese consumer spending will only grow at a moderate pace, endangering expensive consumer stocks (Chart 15). They are at risk of multiple compression when their profits miss elevated growth expectations.

Chart 14

We Downgraded Chinese Offshore Stocks From Neutral To Underweight On Feb 1

| Fullscreen |

Chart 15

Chinese Consumer Stocks Are Rather Expensive

| Fullscreen |

Chinese material stocks have broken down to new cyclical lows (Chart 16). This development heralds new lows in industrial metal prices and commodity currencies.

- Deflationary pressures are acute in China and lower interest rates are warranted. We continue to recommend receiving 10-year swap rates in China.

- Lower interest rates in China, sticky US inflation and a hawkish Fed imply that interest rate differentials will continue moving in favor of the USD. The CNY will depreciate further.

- Chinese currency depreciation will weigh on commodity prices, LATAM and other commodity currencies as well as Emerging Asian currencies.

Our report from two weeks ago argued that the decoupling between strengthening LATAM currencies and falling Emerging Asian currencies and commodity prices is unsustainable (Chart 17). These gaps will be closed via LATAM currency depreciation.

Chart 16

Chinese Material Stocks Are Making New Lows

| Fullscreen |

Chart 17

These Divergences Are Unsustainable

| Fullscreen |

We reiterate our call for a US dollar rally in the coming months. To play this US dollar rebound, we remain short the following currencies versus the US dollar: ZAR, CLP, COP, PLN and IDR. In addition, we continue to recommend shorting KRW vs. JPY, and BRL vs. MXN.

- Consistently, we remain cautious/underweight on EM equities and EM credit markets relative to their DM counterparts.

- EM fixed-income investors should wait for a better entry point. Falling commodity prices are a bad omen for EM credit spreads as well as for EM currencies and, by extension, EM local currency bonds.

Arthur Budaghyan

Chief EM and China Strategist

arthurb@bcaresearch.com