Transitions To Serious Delinquencies Will Cap Credit Card Loan Growth

Consumer credit growth disappointed in June. Total credit outstanding rose by USD 8.9 billion, in June, lower than May's USD 13.9 billion, and shy of expectations of USD 10 billion. Revolving credit (which includes credit cards) declined USD 1.7 billion in June but accounted for the lion’s share of the rise in consumer credit in May.

On a 3-month basis, the New York Fed Quarterly Report on Household Debt and Credit indicates that credit card balances were the main driver of Q2’s overall growth in household debt (+0.6% q/q overall, +2.4% for credit cards). It corroborates reports from the SIFI banks’ Q2 earnings calls that credit cards are generating moderate demand growth.

Consumer credit growth is relevant in an environment of a softening labor market and dwindling excess savings, since it may support consumption growth for longer than we expect and thus push back the start of the recession beyond our current late 2024/early 2025 ETA.

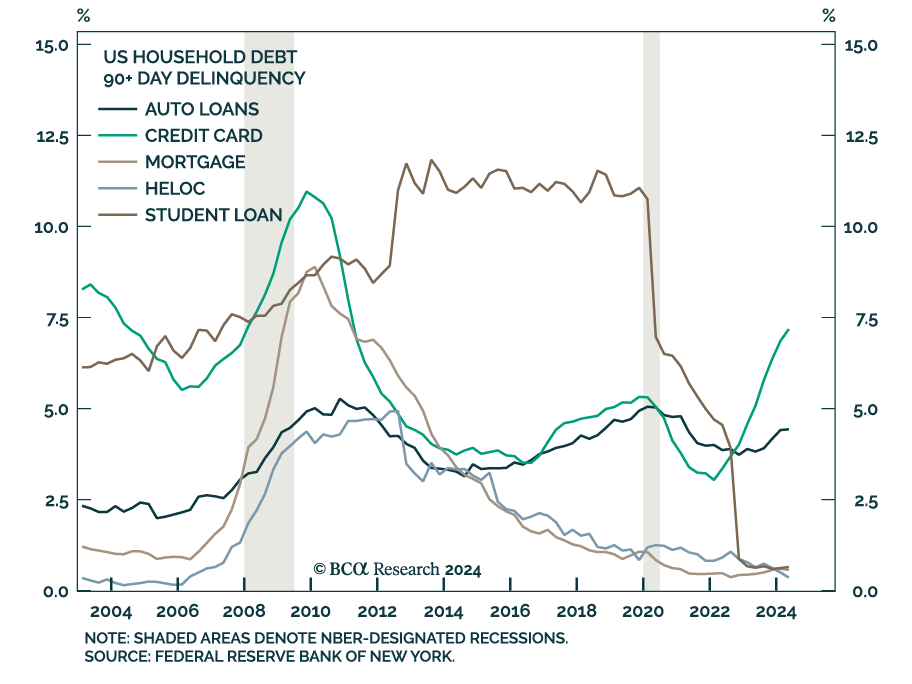

That said, we continue to believe that willingness to borrow will cap credit’s contribution. Lending standards respond to credit performance. Although credit card delinquencies remain low relative to history, they have been steadily rising. Importantly, credit cards’ transition into serious delinquencies (90 days and more) has surged and continued to rise in Q2. Concurrently, the Senior Loan Officer Survey reported tightening credit standards for credit cards in Q2.

Nothing in the recent consumer credit data changes our conviction that the deceleration in labor demand will tip the economy into a recession. Investors should remain underweight risk assets on a cyclical investment horizon.