Investment Implications Of Election and Trump Policies

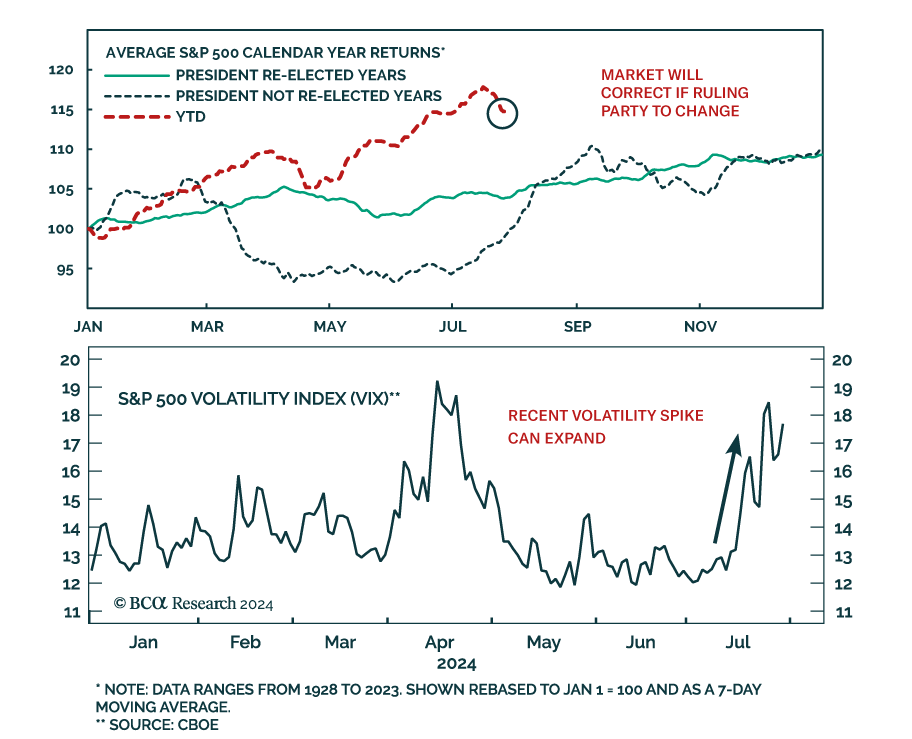

According to BCA Research’s US Equity Strategy service, the stock market outperformance in 2024 thus far is an unusual pattern in election years. The historical data imply that the market will suffer a spill if investors come to believe the incumbent party will change.

The spike in volatility in recent weeks coincided with a surge in the odds of party change (e.g. Republican victory), which confirms this historical framework. Volatility will continue to increase in the near term, especially if the incumbent party fails to regain momentum after changing nominees. Stocks will fall if the incumbent party is poised to fall.

Investors should expect US assets to outperform global peers. By contrast, the market usually rallies after elections, relieved that uncertainty has dissipated.

After the election, the market faces a different question: 2025 will mark a new year with new policies that may or may not affect the markets, depending on the capability and interests of the next government (hawkish or ultra-hawkish trade policy, gridlock or full sweep).

It is impossible to untangle the Trump trade from the ubiquitous expectation of an imminent rate cut and a soft landing. Our hunch is that Real Estate and Homebuilders outperformed for that reason. However, Trump’s immigration reform will be a headwind for the industry as it will increase labor costs, hitting its bottom line.

The Trump trade, i.e. Small Caps, Regional Banks, and Industrials, runs against the BCA view of slowing economic growth that favors defensive assets. And of course, a Trump victory is far from a certainty.