The Sahm Rule Is Not A Leading Indicator For The Economy

Market and economic observers have devoted a lot of attention to the Sahm Rule following July’s employment report, and whether or not it has been triggered. BCA’s analysis has highlighted that the overall direction of the labor market is far more important than the rounding conventions one applies to determine if the unemployment rate has risen enough to meet the exact trigger threshold.

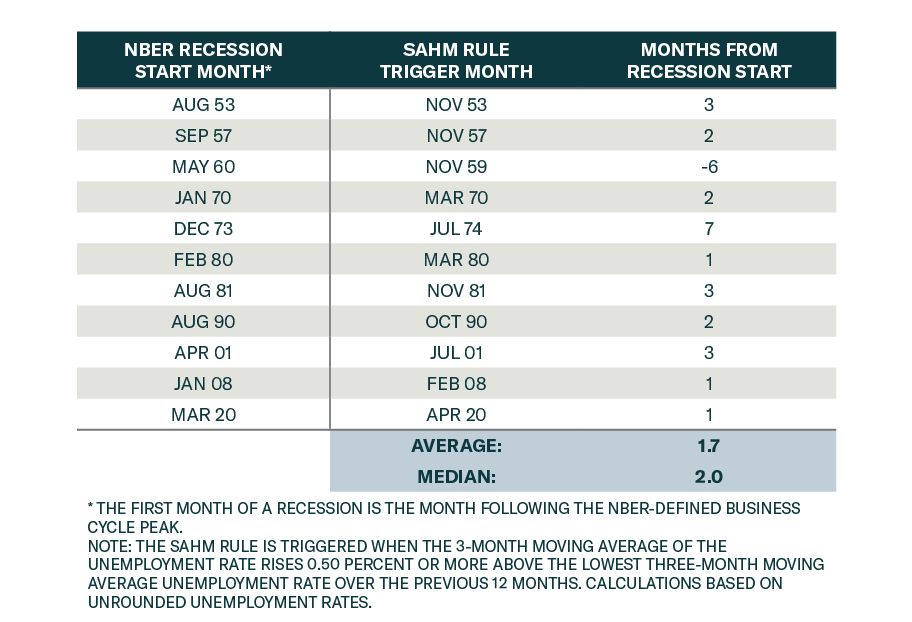

Moreover, investors should keep in mind that the unemployment rate is a lagging variable. Employers typically resort to firing as a last resort. It is therefore worth remembering that the Sahm Rule is not a leading indicator of the economy. Our Global Investment strategists showed that on average, the Sahm Rule has lagged the onset of past recessions by a couple of months.

History therefore suggests that a recession could already be underway even if the Sahm Rule hasn’t been triggered.

Importantly, the hiring rate from the JOLTS report is a more forward-looking indicator. Firms typically stop hiring before they resort to layoffs. Our US Bond strategists also view it as the “purest” indicator of labor demand, since it is not affected by changes in labor supply. The hiring rate has been directionally consistent with a deteriorating labor market for a while.

Households’ perception of labor availability also influences their behaviors and consumption patterns. The quits rate (also from the JOLTS report) and the share of consumers’ assessing jobs as “plentiful” relative to “hard to get” (from the Conference Board Consumer Confidence survey) are both well off their highs.

We continue to expect a recession and are underweight equities. Our conviction is now high enough that our Global Investment strategists have removed their barbell sector strategy (previously overweighting defensives + materials). They are now overweighting defensives outright.