Will Private Investment Save Growth?

BCA Research has been writing extensively on how consumption fueled by excess savings has been propping up the US economy and prevented a recession in 2023. Now, many estimates of pandemic-era excess savings show that they have run out. While consumption is still robust, with June retail sales easily surpassing expectations, its tailwind is likely to wane.

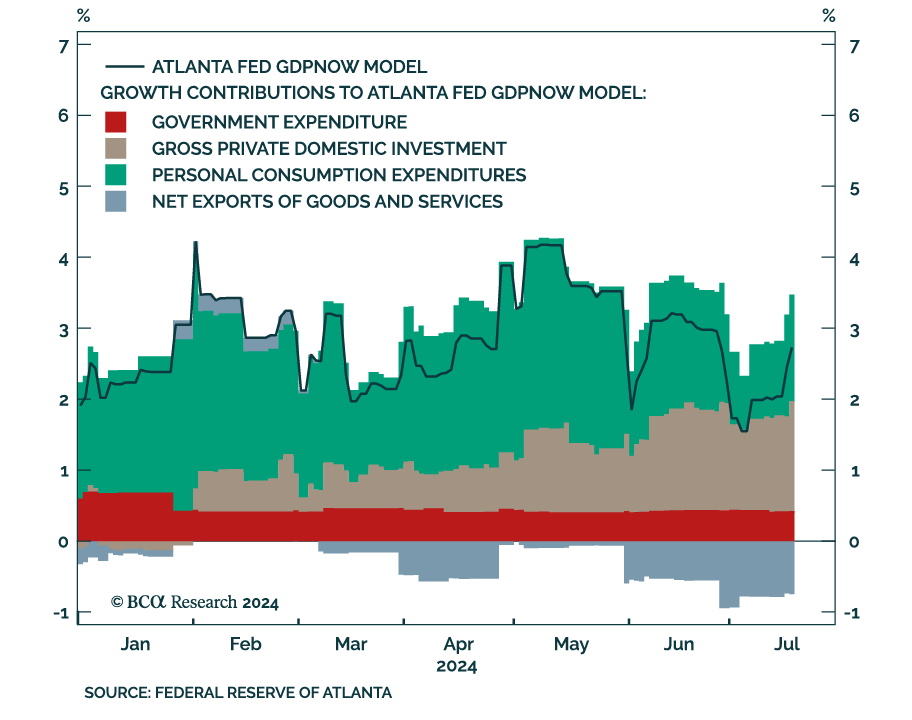

The Atlanta Fed’s GDPNow model corroborates the view that consumption growth will fade slightly. In April – just before the release of Q1 data – the model estimated that consumption would contribute 220 basis points (bps) to real GDP, much higher than the final print of 98 bps, yet still the greatest contributor to growth. Today, it expects consumption to contribute 150 bps to real GDP growth.

Interestingly, the model has been increasing the estimated contribution of investment to GDP growth and anticipates that investment will contribute 155 bps to growth in Q2 at a time when capex intentions are muted, and durable goods orders are slumping. The capex estimate is propped up by anticipated inventory restocking (95 bps), however. Inventory changes should net to zero in the long run and they are not a component of real domestic demand, which is the best growth barometer within GDP.

While our US Investment strategists’ projection that excess savings were exhausted in June was likely too pessimistic, it is becoming increasingly evident that consumers are losing vigor. In addition, relatively tight monetary policy will eventually weigh on capex. Thus, the two private sector domestic drivers of US activity are likely to slow. We continue to expect a recession to begin in the US in late 2024/early 2025.