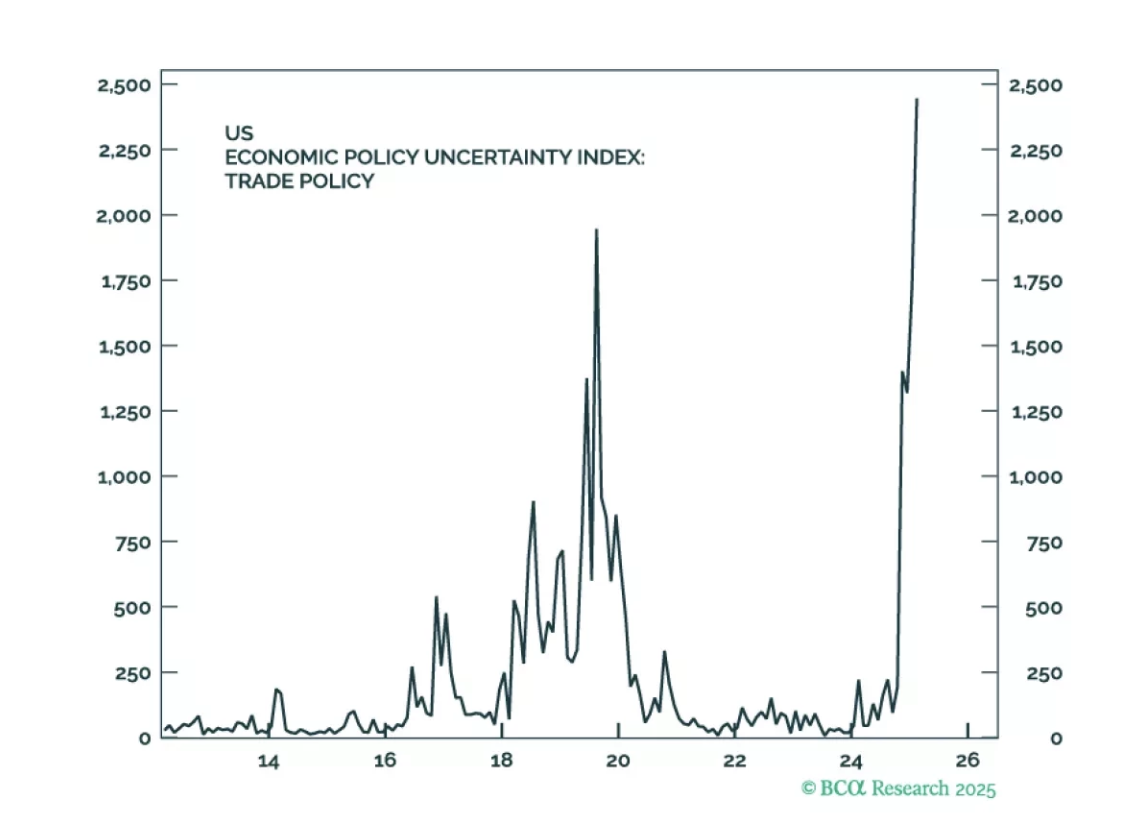

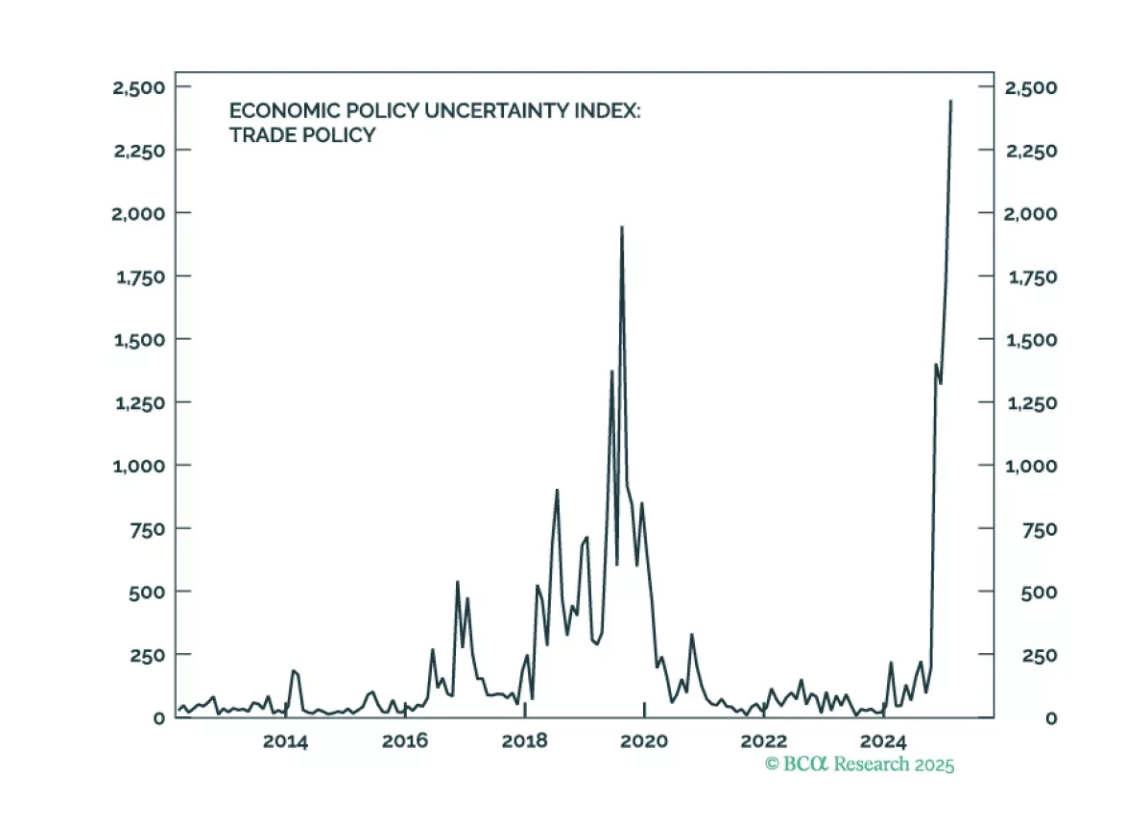

April 2nd Tariff Troubles

Washington’s Trade Playbook Raises Odds

of a Global Recession

BCA Research is preparing for what we call the ''Tariff Trap," where escalating trade tariffs provoke counter-tariffs and raise the risk of a US recession that would exacerbate weak global growth. But tariffs are also negotiable -- and provoke global fiscal stimulus -- so that investors should not fixate on them exclusively.

The administration is spending its scarce political capital on a deeply unpopular issue, and the global bond and currency markets are already signalling investors’ discomfort. The important thing is that the US economy is weakening and China's economy remains in a funk. We summarized below a few of our key conviction views across the spectrum from several BCA Research analysts encompassing US Equities, Fixed Income, Europe and China.

Chief Geopolitical Strategist, Matt Gertken sees the following roadmap:

- Reciprocal tariffs plus Canada suggest the stock market faces further volatility. In the very near term, Trump will focus on Canada, due to its looming election, and will then compromise afterwards. But reciprocal tariffs could push the economy over the edge via trade slowdown and investment uncertainty.

- In the medium and long term, Trump will focus his trade war almost exclusively on China, while settling with US strategic allies. But China's economy is vulnerable and strategic tensions will rise.

Read sample report:

Can Trump Avoid Recession? What About Stagflation?

Our Chief GeoMacro Strategist, Marko Papic complements the view adding:

- April 2 is likely to be the “peak de-globalization hysteria.”, the seven steps of Maximum pressure below describe how President Trump intends to achieve fair trade as tariffs negotiations represent a new baseline.

- A secular dollar decline is likely. Trump’s strategy risks turning the dollar’s traditional role on its head. If tariffs are used to pay for tax cuts, we may be looking at a world that stops treating U.S. assets as safe havens.

- Europe Fiscal Easing: The debt brake would need to be relaxed to fend off declining growth from tightening immigration policy and US tariffs at a time when US fiscal profligacy is also at its peak

- Gold is your insurance. In both soft-landing and hard-crash scenarios, gold stands to gain as the “comeuppance trade” unfolds.

Read sample report:

April 2: Sell The Rumor, Buy The News?

A Recession is Imminent?

- Our Chief Global Investment Strategist Peter Berezin raised odds of a US recession in the next 12 months from 65% to 75%. Weaker data from job openings & unemployment, excess savings and credit delinquencies are rising to the fore, especially with commercial real estate.

- We are underweight global equities.

Analysis Paralysis

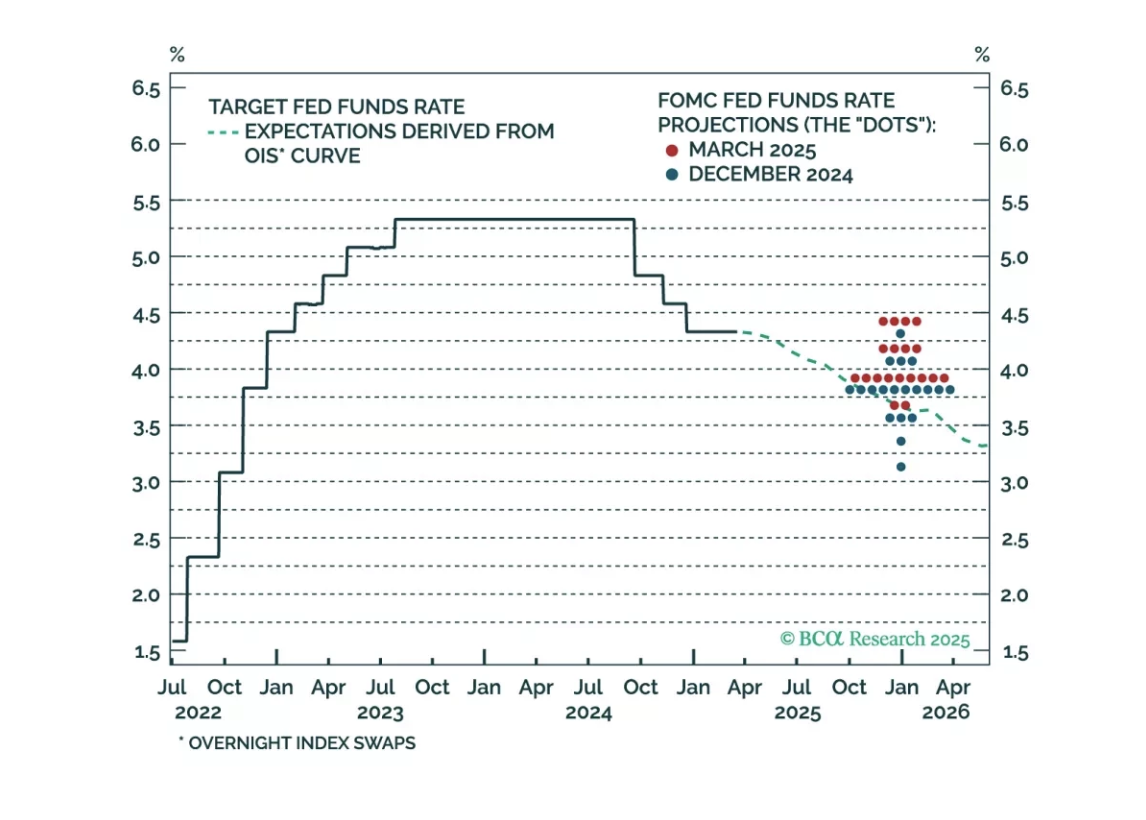

- The current US Treasury bull steepening reaction after the latest Fed meeting also seems mispriced. Our US Bond Strategist Ryan Swift thinks the Fed will not simply look through the impact of tariffs on inflation and straightforwardly proceed with 50 bps of easing this year.

- We continue to maintain above benchmark US portfolio duration and Treasury curve steepeners over 6-12 months.

Keeping an Ear to the Ground: What are US Companies saying about Tariffs?

- Our Chief US Equity Strategist Irene Tunkel commented that earnings guidance have been deteriorating fast, and the strong dollar has been pounding multinationals.

- Technology and Consumer Discretionary sectors are already under pressure, and banks are bracing for a rise in delinquencies.

- We are underweight US banks and Diversified Financials, as well as the Consumer Discretionary and Technology sector, while favouring Utilities, Pharmaceuticals and Telecoms.

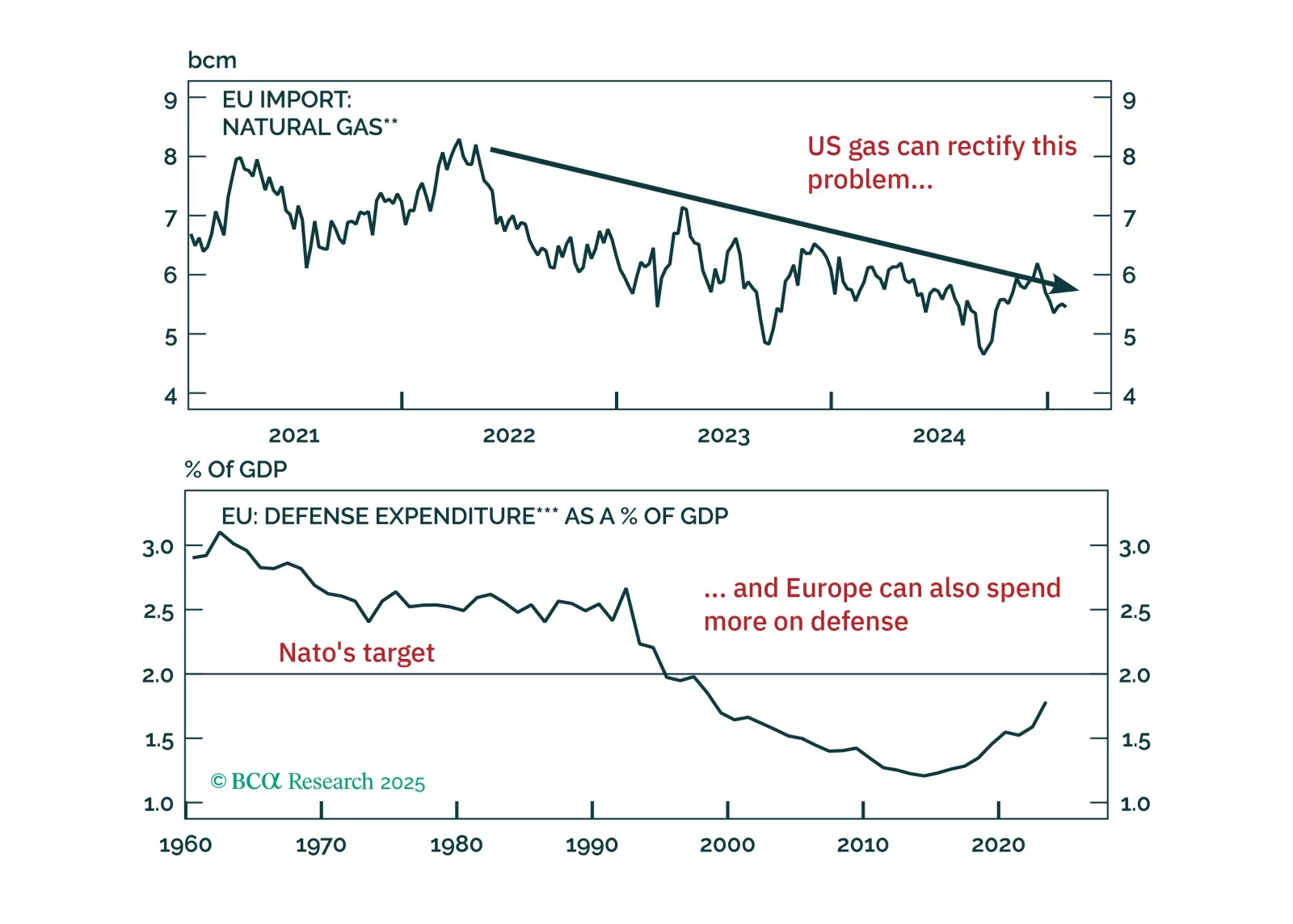

Europe Is Next

- Our European Investment Strategist Mathieu Savary argues that the uncertainty created by President Trump’s trade war is already weighing on European economic activity via falling capex.

- Combined with tighter financial conditions following the surge in German yields since February, this cocktail increases the odds of a Eurozone recession this year.

- However, not all is negative. Trump’s threats are also forcing European authorities to ease fiscal policy, to work on integration, and address structural deficiencies of the Eurozone.

- As a result, pullbacks in European assets create attractive long-term opportunities for investors.

China: Bracing For The Impact Of Tariffs

- Finally, Jing Sima believes that U.S. tariffs on Chinese exports, now exceeding 30%, could reduce China’s 2025 GDP growth by 0.5 to 1 percentage point and further weaken the RMB towards 7.4-7.5 against the dollar by Q3 2025.

- While Beijing is prepared to provide economic support, any stimulus is expected to be reactive rather than proactive, likely triggered by clear signs of slowdown or market stress. In the event of severe strain on manufacturing or employment, China may offer targeted subsidies similar to those used during the previous trade war, equivalent to about 1% of 2018-2019 GDP to cushion the export sector.

- For now, investors are advised to avoid Chinese equities until the tariff impact becomes clearer, though onshore stocks are preferred over offshore ones due to stronger domestic policy backing.

About BCA Research

BCA Research is the leading independent provider of global investment research. Since 1949, BCA Research’s mission has been to shape the level of conviction with which our more than 2000 clients make investment decisions, through the delivery of leading-edge top-down analysis and forecasts of all the major asset classes and economies, including Private Markets and Alternatives.

Our team of 60+ researchers and chief strategists all have rich background experiences at top tier sell-side and buy-side institutions.