China Needs Fiscal, Not Monetary Easing

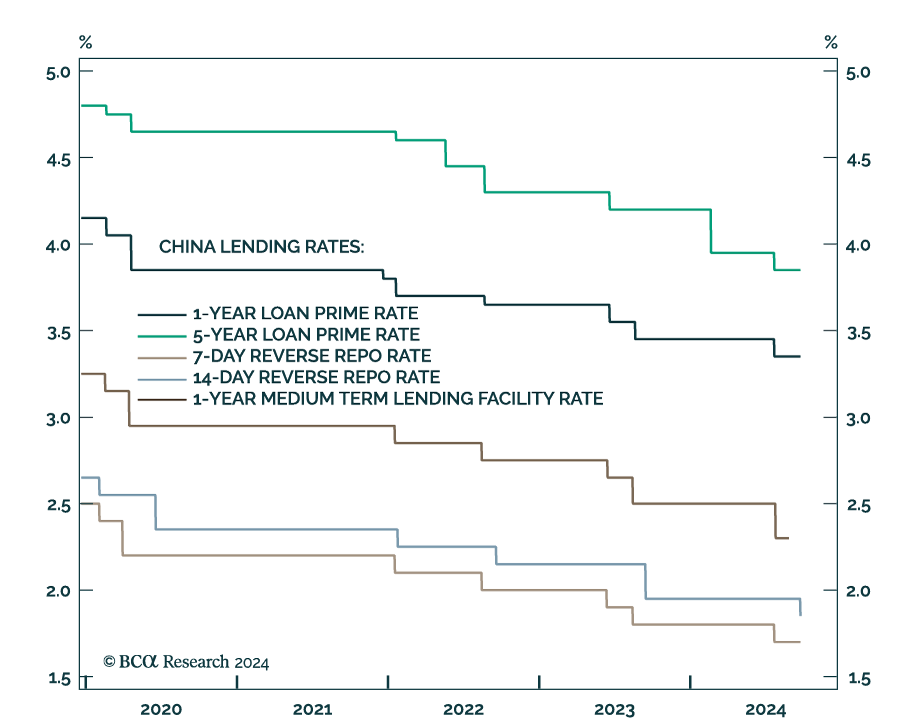

The PBoC lowered the 14-day reverse repo rate by 10 bps on Monday, a move that follows a string of easing measures in late July when the central bank lowered the 7-day reverse repo rate, several maturities of the loan prime rate and the 1-year medium-term lending facility rate.

Our China Investment strategists highlighted that given their small magnitude, this week’s and July’s cuts are unlikely to move the Chinese growth needle. Additionally, already low rates provide little scope for monetary policy to meaningfully impact the economy. Moreover, they view this week’s cut as a mere seasonal boost (end of quarter, beginning of the Golden Week).

Our colleagues nevertheless expect a more meaningful monetary policy easing package before the year is out. Notably, they assign high odds to policymakers reducing interest rates on existing mortgages. Existing homeowners currently pay higher mortgage rates (4.27% on average) than new home buyers (3.45% on average), and the PBoC move would align existing and new mortgage costs within a range of 3.27% to 3.47%.

They expect this gesture could potentially lift private sector sentiment in the mainland economy. However, absent a turnaround in the labor market or meaningful fiscal stimulus targeting household disposable income, this revival in sentiment is likely to be transitory.

Domestic demand is likely to remain muted, while external demand headwinds will constrain Chinese exports. That said, although the Chinese economic outlook remains bleak, cheap valuations cushion Chinese equities on the downside. Investors should overweight and equal-weight onshore and offshore stocks, respectively, relative to global equities.