Elevated Equity Multiples Point To Low Long-Term Returns

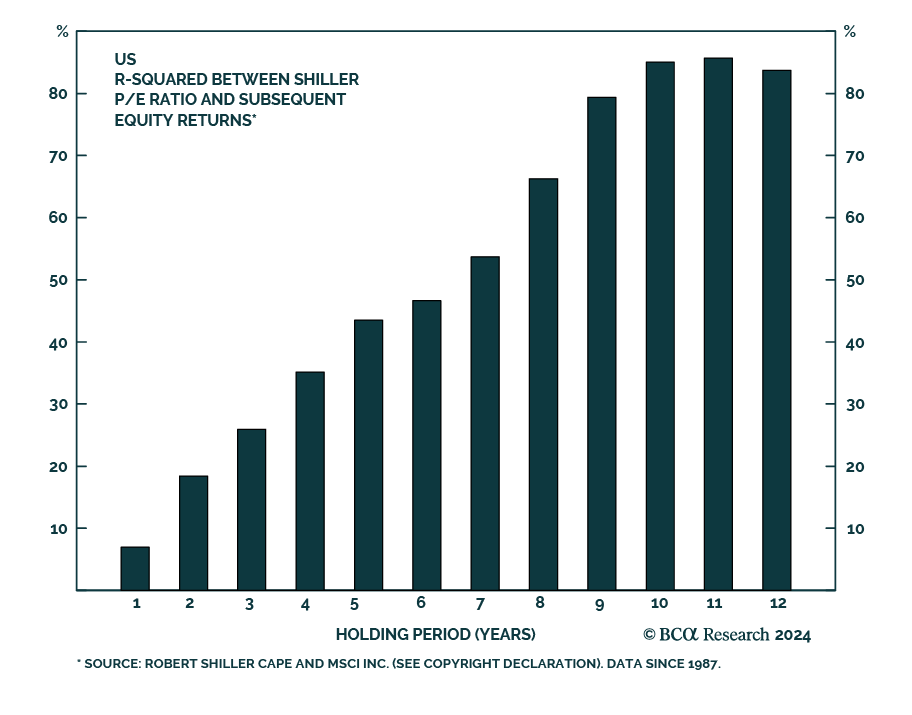

Elevated US equities valuations and their impact on returns are a hot topic right now. Valuations are not a tactical or cyclical timing tool, but they help predict long-term returns. Our Global Asset Allocation Strategy team publishes their multi-asset 10-to-15 years return assumptions annually, and this year’s edition points to a strategic underperformance of US equities vs. its DM peers.

Valuation is one of their inputs, and is the main factor dragging projected returns for US equities. While their calculations point to a 3.2% annualized return, other DMs should see 5.1% returns. These numbers are below historical averages, and show a reversal of the massive US outperformance from recent decades.

Our colleagues discussed the matter during our BCA Live & Unfiltered meeting, delving into whether this dim outlook applied outside of megacaps. We think growth stocks will underperform value stocks as investors book gains when the next recession comes.