Eurozone CPI At 3-Year Low Paves Way For September Cut

After surprising to the upside in July on higher energy costs, Eurozone CPI resumed its deceleration in August. Headline and core CPI declined from 2.6% y/y to 2.2% and from 2.9% to 2.8%, respectively.

Energy prices contracted 0.3% y/y from July’s 1.2% increase, however services inflation, which is more sensitive to domestic economic conditions, ticked 0.2 ppts higher to 4.2% in August.

The Eurozone economy is ultimately fragile. The labor market is deteriorating, bankruptcies are rising rapidly, construction activity has collapsed and the private sector’s interest burden is rising. The external landscape is also inauspicious. We expect the US will enter a recession in the next 6-to-12 months and China’s efforts to stimulate its economy will be insufficient to meaningfully revive Chinese demand for Euro area exports.

Therefore, we expect disinflationary forces to dominate the Eurozone growth landscape on a cyclical investment horizon. Our European Investment strategists expect the ECB to cut twice this year, in September and in December, mostly in line with market expectations.

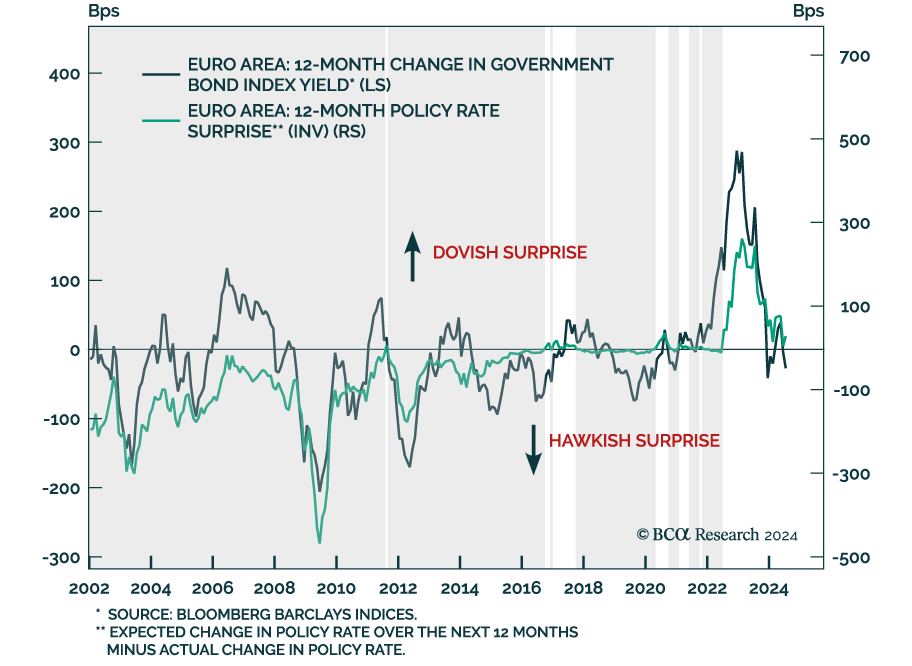

That said, they expect the central bank to ease more aggressively next year when the Eurozone is more likely to experience a recession. A dovish surprise is supportive of Bund prices and investors should overweight them on a 12-month investment timeframe.