Recession Remains Our Base Case

One key takeaway from Wednesday’s post-FOMC press conference is the Fed’s unshaken conviction that it can avoid a recession. A risk-on mood dominated markets on Thursday, with the S&P 500 breaching new all-time highs while the 10-year Treasury yield rose 3.5 basis points (see Indicator Spotlight).

This week’s economic data releases were also resilient-to-positive. Industrial production expanded in August and the first two September regional Fed manufacturing surveys sent a positive signal. The August retail sales underscored mixed details but were overall not consistent with an imminent recession, and housing starts bounced back in August.

Still, we are not ready to abandon our US recession call on a 12-month horizon.

First, it hinges on the labor market and its passthrough to consumption. Ongoing softening in labor demand will continue to exert downward pressure on wage growth and attenuate the boost from household spending’s main driver at the same time as other consumption tailwinds are fading.

Second, aggressive rate cuts do not materially alter this expectation because monetary policy works with a lag. Current conditions are the product of past tightening and current cuts may only ripple through the economy after it is already too late.

Third, this week’s 50-bps cut keeps monetary policy restrictive. The Fed funds rate remains above even the Fed’s own estimate of the neutral rate.

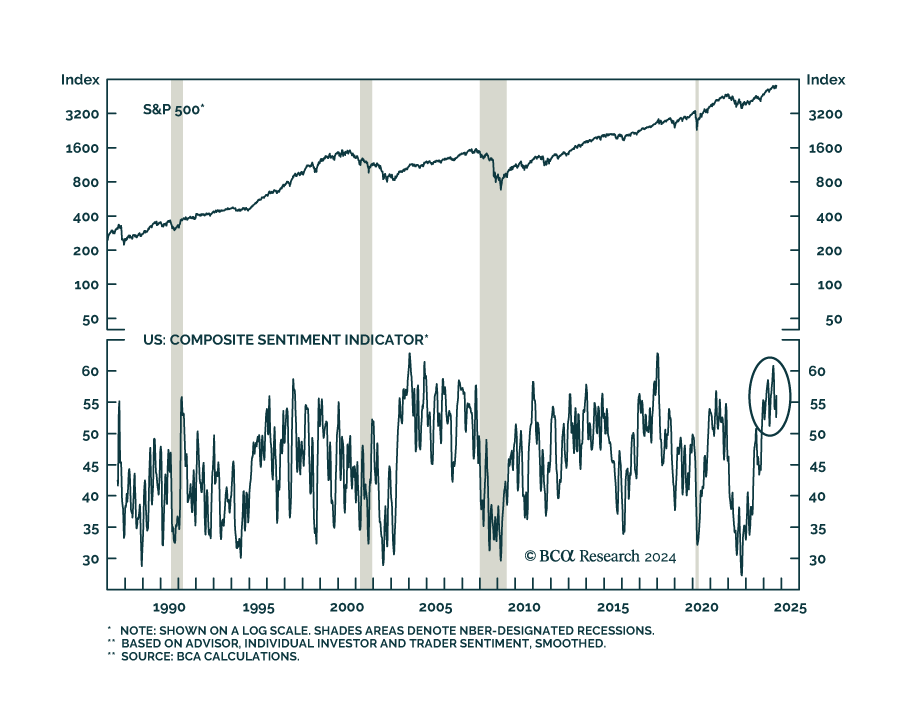

Nevertheless, our subjective odds for a recession in 2024 have decreased and stocks may still rise in the short run as investors continue to expect a soft landing. Further gains will only make equities more vulnerable to the downside.

We are thus reluctant to chase equities higher and remain underweight.