What Could Durably Reverse US Equities’ Relative Outperformance?

According to our Bank Credit Analyst service, an inflection point in the relative performance of US stocks is not likely to occur over the coming 6-12 months. A recession favors US equities in common currency terms barring substantially less global ex-US earnings weakness than has historically occurred, or highly atypical recessionary behavior from the US dollar.

Over the longer term, US equities’ relative outperformance is long in the tooth. Even if US stocks outperform their global ex-US peers during the next recession, it will occur due to an outsized global ex-US earnings decline that will ultimately reverse. But the US equity multiple compression which will occur during the next recession may be permanent, unless lofty expectations about AI’s potential to impact economic activity are met.

Investors’ expectations about AI’s positive impact are extremely aggressive. Our colleagues estimate that investors are expecting the deployment of AI technology to catalyze a 10-to-20-year productivity surge along the order of the IT revolution of the 1990s, with persistently high margins on the revenue generated from the improvement in growth. While artificial intelligence technology will likely lead to new revenue growth for some firms, these extraordinary aggregate expectations are not likely to be met.

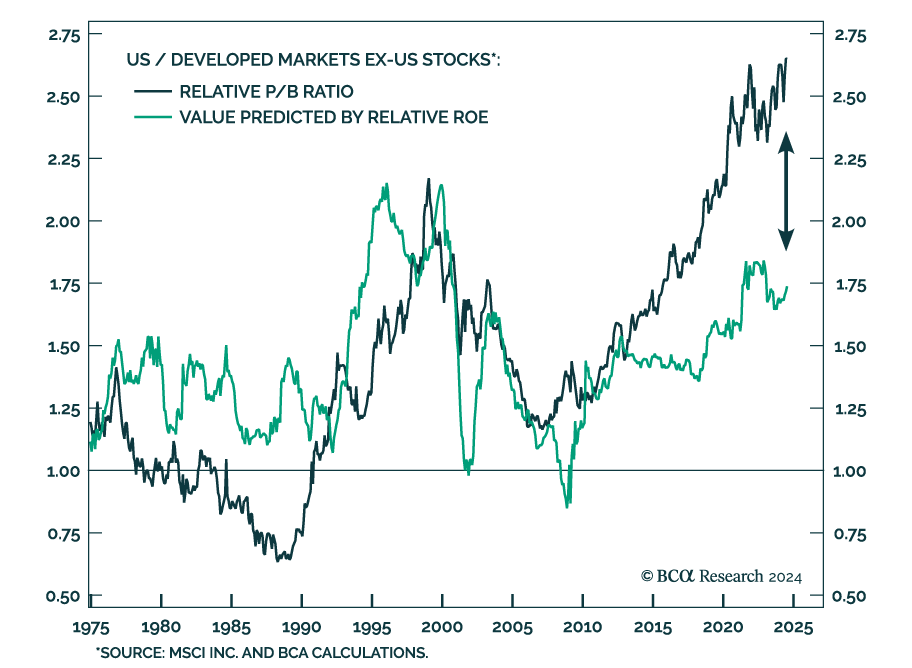

Moreover, US return on equity is very elevated compared to global ex-US stocks, which underscores the risk to US earnings. Return on equity is a function of profit margins, asset turnover, and leverage. While US firms are likely more efficient than their global peers at generating revenue from assets, the rise in US ROE has been significantly driven by rising profit margins which now appear very stretched historically. Even if rich US profit margins are sustained at current levels, US equities are still overvalued given the historical relationship between relative multiples and relative ROE.

Does this mean that global ex-US outperformance is likely over a structural time horizon? Not necessarily. It may just mean that the US will stop outperforming, potentially with relative multiple compression cancelling out a better relative earnings profile.