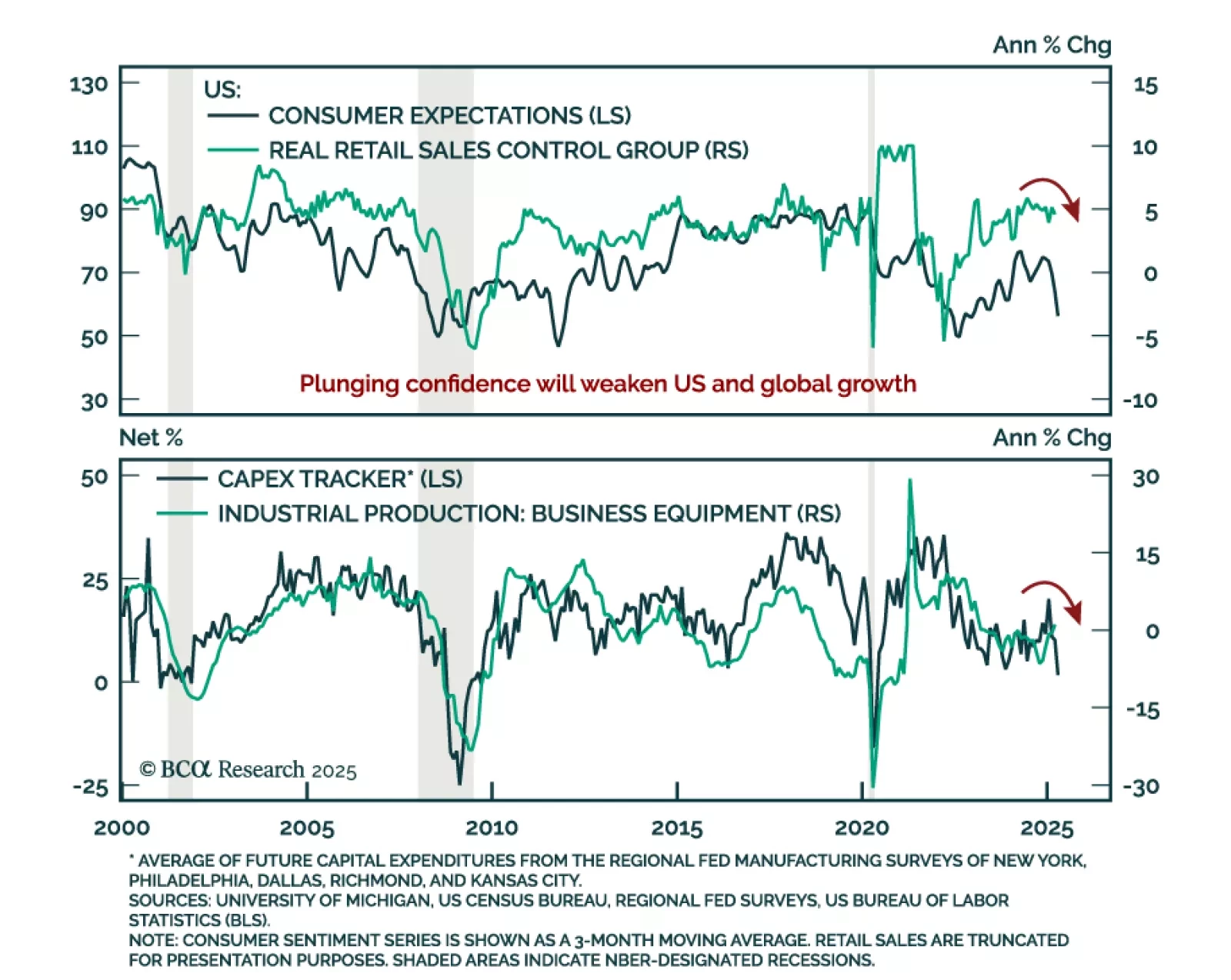

Will US Hard Data Soften?

Soft data continues to deteriorate and hard data will soon follow, reinforcing our defensive asset allocation. Consumer and business confidence have plunged as policy uncertainty and inflation expectations rise, with spending, hiring and capex plans softening.

March retail sales were decent but mixed: Headline growth was strong at 1.4% m/m, but the control group missed at 0.4%, down from 1.0%. Core sales excluding autos and gas rose 0.8%, suggesting some frontloading ahead of tariffs. Restaurant sales held up, but downside risks remain high as uncertainty lingers and confidence falls, which will lead to a higher saving rate.

Industrial production declined 0.3% m/m, with capacity utilization falling to 77.8%. While hard data has yet to show a deep slowdown, leading indicators suggest weakness is coming. Given those risks, we remain underweight risk assets, and overweight government bonds.