Download Report

Please complete form to access this report

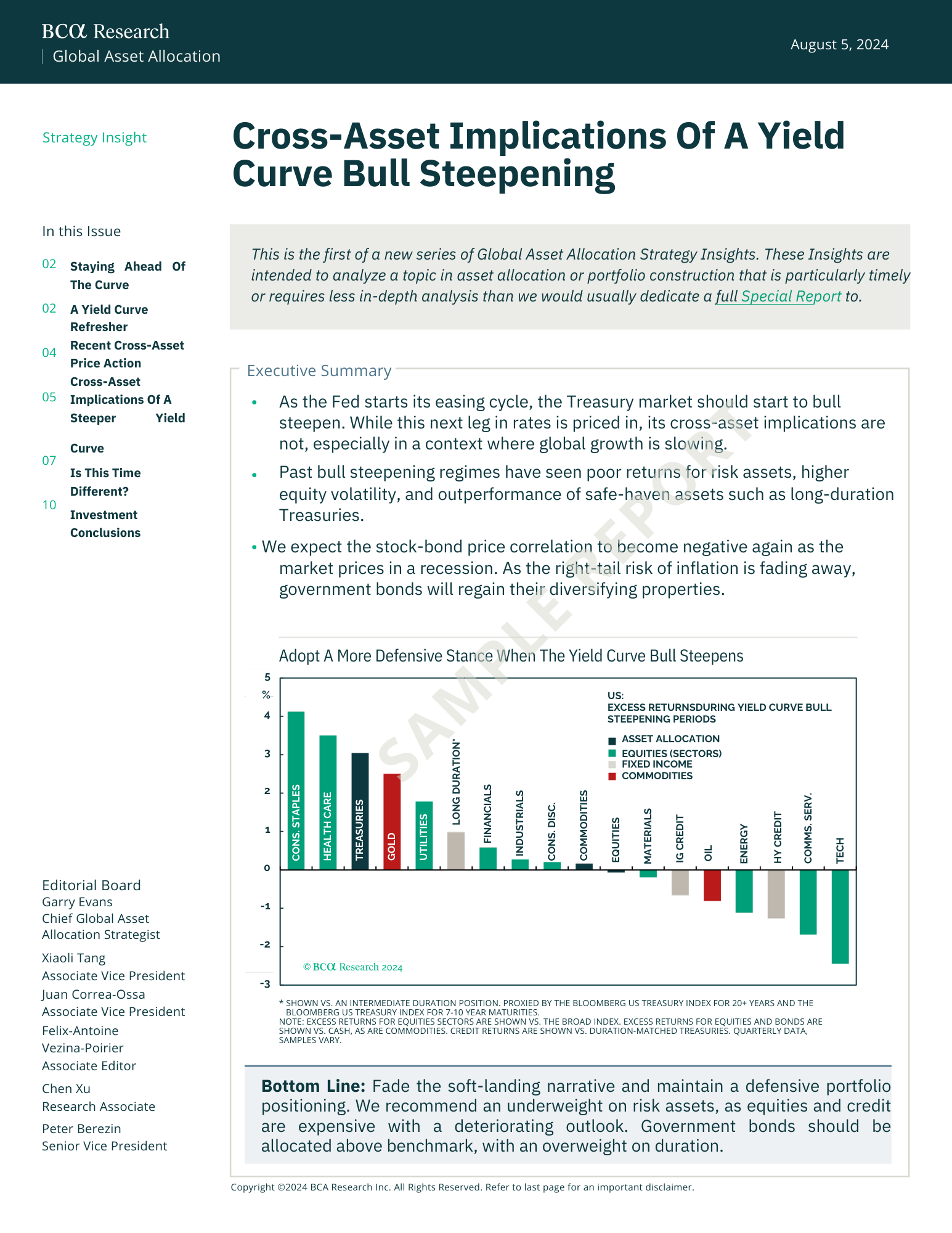

As the Fed starts its easing cycle, the Treasury market should start to bull steepen. While this next leg in rates is priced in, its cross-asset implications are not, especially in a context where global growth is slowing. Past bull steepening regimes have seen poor returns for risk assets, higher equity volatility, and outperformance of safe-haven assets such as long-duration Treasuries. We expect the stock-bond price correlation to become negative again as the market prices in a recession. As the right-tail risk of inflation is fading away, government bonds will regain their diversifying properties.